This blog posting opines on what might lie ahead for the Patient Protection and Affordable Care Act (aka Obamacare). In a previous posting, I commented on the unlikely case for total repeal; the musings below address where potential resolutions might exist and where they will be difficult to obtain.

There appear to be several principles upon which political partisans might agree regarding health policy reform in the U.S.

- Affordable insurance should be available to all eligible residents.

- No one should be denied access to affordable insurance as a result of a pre-existing condition.

- A market for the purchase of individual/family health insurance should be viable.

- Children should be able to stay on their parents’ policy until age 26.

- The growth in the cost of medical care needs to be brought down to a rate closer to that of the national economy than it has been in the last few decades.

- Eligible residents should have choice in the type of insurance plan they desire, and thus, be able to make tradeoffs among what they pay for the policy, the magnitude of the deductible, payment levels for services, and the breadth of the network of providers they wish to access.

There exists substantial disagreement about how the above principles might be addressed including:

- The relative roles of states and the Federal government in organizing and regulating markets

- How physicians and other medical care providers should be paid

- Requirements for what “affordable” insurance must cover (e.g., the 10 essential benefits existent in the ACA)

- The character of subsidies/penalties to encourage purchase of insurance – credits vs. deductibles, income related or fixed independent of income, age-related or not

- The method to be employed to discourage the purchase/use of services that are expensive and yield at best small improvements in health status.

- Whether Medicaid and Medicare should be distinct programs funded through separately designated sources or integrated with private options for the purchase of health insurance

Various Republican politicians have proposed plans for the repeal of Obamacare. Each option generates significant consequences for patients, providers, and payors.

Replace then repeal, which could be characterized as reform of the ACA, however, could both improve health policy – in terms of delivering on the principles noted above – and serve politicians need to argue that they have repealed Obamacare. The labeling can be left to our prospective chief executive labeler. In a recent Milbank Quarterly Op-Ed piece, however, Gail Wilensky explains why politics and constructive policy are likely to be incompatible. She concludes as follows:

“The forces for ‘repeal and figure out next steps later’ may be too great for serious, bipartisan legislation – even if it complicates the ultimate goal of ‘repeal and replace.”

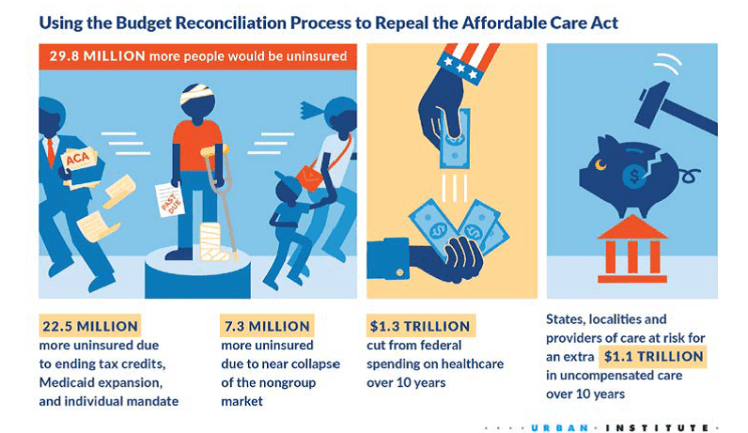

Through the budget reconciliation process, which only requires a majority vote in each house, Congress could enact a bill similar to the one it passed in 2016 (and vetoed by President Obama.) Such legislation would remove funding for premium tax credits used in the exchange, funding for Medicaid expansion, individual and employer mandated purchase and penalties, the medical device tax, the insurance tax, the tax on high-cost insurance plans (the so-called “Cadillac tax”), and increased taxes on the wealthy to pay for Medicare. At least 20 million people would no longer have health insurance, the individual insurance market would likely collapse (from adverse selection and rising premiums for those who remain), uncompensated care provided by physicians and hospitals would rise, and health insurers’ revenues would fall. The below figure characterizes the Urban Institute’s view of the consequences of such a partial repeal.

According to the Urban Institute’s simulation model, nationally, the number of uninsured would more than double with the result of more people and a higher percentage uninsured than prior to the ACA. Thirteen states would see at least a 150% rise in the share of its population who lack insurance; these include Arkansas, Iowa, Kentucky, Louisiana, Michigan, Montana, North Dakota, Ohio, and West Virginia – all states won by President-elect Trump. Given the shared principles noted above, a bill similar to that passed in 2016 (given the certainty at the time of an Obama veto) would by highly unlikely.

If replace then repeal were to be the objective – not inconsistent with either the goals of President-elect Trump or the “Better Way” plan posited by House Speaker Paul Ryan and others – then fixing some of the major deficiencies of the ACA would be in order. These include, but are not limited to, inadequate incentives for the young and healthy to purchase health insurance – even with the penalty for non-compliance, poorly designed and funded risk adjustment/ fund transfer and re-insurance provisions, lack of competition in both the health insurance and medical provider markets in many regions, and the unpopularity of some of the funding provisions and purchase mandates. Alice Rivlin, Loren Adler, and Stuart Butler have addressed what might work here. These and other approaches will be topics for future postings.