As T. R. Reid points out in his marvelous new book, A Fine Mess, fundamental tax reform in 2018 is due if we are to follow the major reform every 32 years established in the 20th Century (with such reforms in 1986, 1954, and 1922.) The 1986 reform was exemplary in many ways; let me cite two specific ones: 1) it adopted the strategy of building a broad tax base with very limited exemptions which allowed for the adoption of a small set of relatively low rates and 2) it required bi-partisan support including valiant efforts by Senators Bradley (D) and Packwood (R) along with the signature of President Reagan.[1] Reid devotes an entire chapter to the attraction of broad based, low tax rate structures (BBLR for short), and this posting argues that such a structure can meet a set of principles that would attract consensus support.

The proposals presently passed by the House of Representative and by the Senate share neither of the aforementioned attributes of the 1986 reform. For a detailed comparison of the proposals see The Daily Signal . This posting follows the argument that I described in a previous posting with regard to health policy reform (); reform based on shared principles differs markedly from one based on competing stakeholder interests.

As background, it is worth noting several key features of the current income tax structure. See the Tax Policy Center for details.

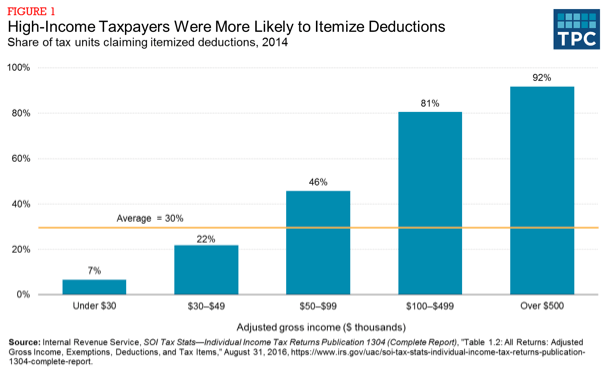

- Only 30% of households itemize and thus take advantage of deductions and exemptions such as those for mortgage interest payments and state and local property taxes. See the chart below.

- Tax expenditures (including deductions and exemptions as well as an array of tax credits) substitute for spending programs that reduce (and thus redistribute) the tax burden; they sum to more than $1.5 trillion based on OMB budget outlay estimates for fiscal year 2018, roughly equivalent to what is collected with the federal income tax. 28% of these benefits accrue to households in the top 1% of income levels and 50% benefit the top 10% of such households.

- Little in the way of base broadening is offered in the bill passed by the U.S. Senate. Only limits on state and local government tax deductions are addressed in the Senate bill. According to the U.S Treasury Department, they account for less than $100 billion of foregone tax revenue.

Clearly, the existing tax structure falls far short of a “good” system, which I describe below. Tax reform is clearly needed, though not necessarily the one(s), as far as anyone can tell, that are presently under consideration. The first Chancellor of Germany Otto von Bismarck noted that “Laws are like sausages, it is better not to see them being made.” Economist Eugene Steuerle further argues that “It is never truer than with tax legislation, and Tax Cuts and Jobs Act is no exception.”

Shared Principles and Values

Discussion of the principle requirements for a “good” tax structure go back at least to Adam Smith. In simple terms, a good tax system should be fair in its distribution of the burden, efficient in resource use, be consistent with sustainable macroeconomic policy, and be easy to both comply with and administer. (See the fifth edition of Taxing Ourselves: A Citizen’s Guide to the Debate over Taxes by Slemrod and Bakija for a comprehensive analysis.) Based on these characteristics, virtually no one would characterize the U.S. income tax system as “good.” Consider the following principles:

- A “good” tax system should fairly share the burden of paying for governmental goods and services. Economists interpret fairness in terms of horizontal and vertical equity.

- Horizontal equity can be interpreted as follows: tax paying units (for example, individuals or families) in similar circumstances should pay similar amounts. Thus neither the source of income nor the expenditure patterns that people choose should affect their share of the burden of the income tax.

- Vertical equity requires a value judgment about the distribution of the burden of taxation. Based on ability to pay, those with more income should pay at least proportionally more than those with less income (taking into account appropriate differences such as family size.)

- Based on the comprehensive concept introduced by Haig and Simons: in a given year, income should be defined as “the change in an individual’s power to consume during that year.” It should not be dependent upon whether the income comes from labor or capital. Some forms of income, such as for the carried interest received by some firm owners and fund managers, cannot easily be segmented into labor and capital components.

- A “good” tax system should encourage efficient resource use. Economists interpret efficient use as activities that would result in a system with neutral taxes, that is, one in which taxes neither encourage nor discourage particular forms of income or expenditure. Economic behavior that is not responsive to changes in tax-adjusted prices (inelastic demand or supply) would satisfy this criterion; however, building a tax system solely on this basis would likely generate vertical inequities, since low and moderate income families may not be able to easily change their behaviors in light of increased taxes and thus would bear an increased burden relative to high income families.

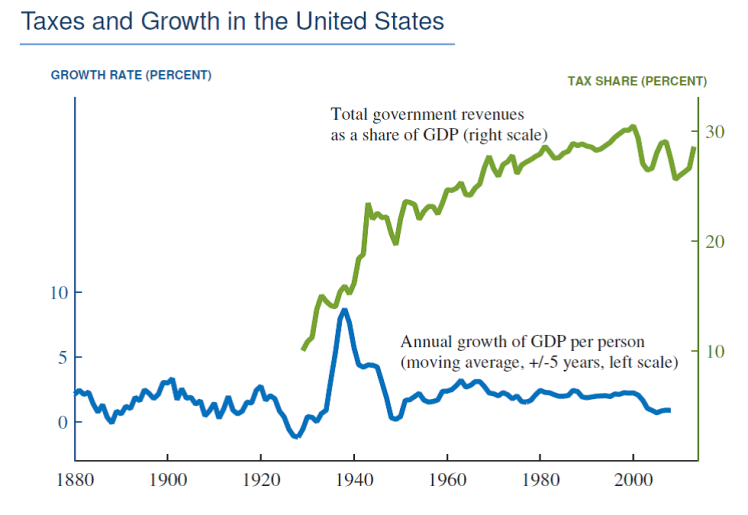

- A “good” tax system should be consistent with sustainable macroeconomic policy. Obviously, there are many complexities and choices related to such policy as regards the welfare of the population of a country. Here, I will focus solely on its ability to generate economic growth. Many assertions have been made about the relationship between income taxes (especially the marginal tax rate structure) and economic growth. The literature on economic growth makes little mention of an independent role for taxes per se. For example, the Penn Wharton Budget Model projects that the bill will raise the level of GDP in 2027 by less than 1%. (t) Charles Jones, a Stanford economist who specializes in both theoretical and empirical explanations for differences in economic growth rates across countries and time, provides the graph below to illustrate the lack of a relationship between the aggregate rate of taxation and the rate of economic growth in the United States over the past century.

Note that governmental revenue as a percentage of GDP grew steadily between 1930 and 1980 with average growth of Real GDP per capita largely unchanged except for the Great Depression and World War II period. In the last decade both governmental revenues as a percentage of GDP and GDP per capita growth have declined.

- The cost of both administering and complying with a tax system should not be burdensome. Though I won’t provide an estimate of the magnitude of such burdens, given the hours and resources spent by both filers and the IRS, few would disagree that our system, given its complexity generates huge burdens on the population.

This aggregate picture of the U.S. economy doesn’t say that the character of the tax system doesn’t matter, but it does suggest that the level of taxation may not be a critical driver of economic growth. Jones ( argues that the character of the social infrastructure including the ease of both establishing and closing down a businesses, the physical infrastructure (e.g., roads, transit, water, sewerage), the availability of a healthy and educated work force, and well defined and enforced property rights matter more than the level of taxation. To the degree public funding is necessary to support such social infrastructure, a tax system perceived as fair and efficient must be in place. Clearly, such is not the case with our current system and as Steuerle argues, the tax reform proposals under consideration are unlikely to improve on either count.

Constructive tax reform should employ the principles noted above which are consistent with the “broad base, low rate” structure emphasized in Reid’s book. A “good” tax system is less related to how much is raised in taxes than to the absence of distortions to economic activity built into the system and the existence of sufficient revenue raised over time to meet the aforementioned social infrastructure needs. Of course, the character of the taxation of capital matters in both encouraging economic activity and fairly distributing the burdens of our social infrastructure. I plan to devote a future blog posting to the taxation of capital in general and the corporate income tax in particular. In summary, although there are some constructive aspects of the tax reforms under consideration, the proposed changes do much more to redistribute the burdens of a civilized society than to improve our responses to such burdens. Stated differently, and consistent with the title of this posting, the character of the tax reform proposals passed by both houses reflect a responsiveness to particular stakeholder interests (such as large companies and high income households) rather than to a set of shared values.

[1] This bill initially passed the U.S Senate by a vote of 97 – 3 despite the elimination of deductions for sales taxes and for interest payments unless they could linked to a home equity loan.

Thank you for this lucid, detailed, and articulate overview. Clarity and facts are in short supply in the current claims and arguments about what “tax reform” looks like.

LikeLike