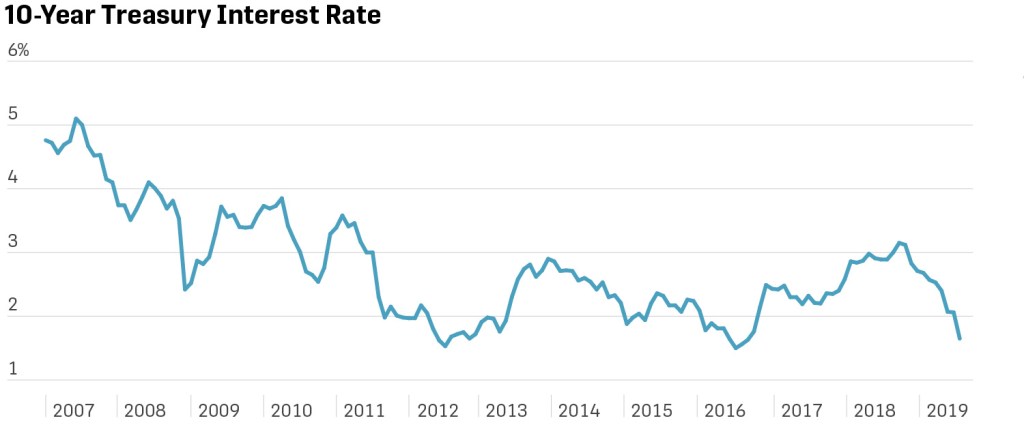

This piece was originally posted on the Lawrence Economics blog in 2012. This version has been updated in many places; however, the effects discussed in that posting remain a major concern today. Political pressure to not only keep interest rates low but to lower them further seem unstoppable, especially since the eventual economic consequences are not easily attributable to contemporary advocates such as the President.

Satyajit Das, in the January 12, 2012 edition of the Financial Times, argued that low interest rates generate a variety of economic distortions that expand rather than address structural problems in economies (whether those of the U.S., Europe, or elsewhere.) These effects are especially pernicious when real interest rates (that is market interest rates minus the expected inflation rate) are negative. He provides a laundry list of “side effects” to this economic drug of choice.

1. Encourage the substitution of capital for labor: Is it any surprise that employment was slow to respond to the monetary stimulus provided to help the U.S. economy escape the Great Recession from 2007 to 2009? Even though GDP at the end of 2011 was higher than it was at the beginning of the last recession, employment was far below its previous peak and did not fully recover until the middle of 2014.

2. Encourage the substitution of debt for equity funding

3. Discourage savings, especially when real rates are negative: Of course, if households have a particular wealth target, low rates could induce additional savings.

4. Create a funding gap for defined benefit pension plans: Plan managers either must reduce benefits or attempt to increase returns through more risky asset purchases)

5. Feed asset price inflation through the purchase of risky assets (related to point 4)

6. Reduce the cost of holding money: This inhibits the flow of capital to more worthwhile activities.

7. Allow banks to borrow cheaply (from depositors) and achieve their income targets through purchase of governmental securities rather than through lending to the private sector: Such bank behavior is made especially easy when the FED pays a higher interest rate on all bank reserves than CDs offer savers. For example, presently (September 1, 2019), the FED is paying 2.1% on reserves; while, five year CDs offered by banks typically offer much less than 1%.

8. Distort currency values as deviations in interest rates across countries: Differences in interest rates are one of the drivers of short term capital flows.

9. Induce a reliance on low interest rates to continuously fuel aggregate demand: Given the lengthy period of low (nominal and real) interest rates and the relatively high uncertainty regarding macroeconomic stabilization policies, the influence of changes in interest rates is likely to be very small.

For the most part, those who argue for extended periods of low interest rates believe that aggregate demand drives aggregate output. They tend to underplay the importance of structural change in the economy (such as labor market, regulatory, trade or tax policy reform); such change cannot be addressed by replacing depressed elements of aggregate demand with monetary policy induced aggregate spending. The day of reckoning is just extended, not cancelled. Just ask the Europeans or the Japanese.

It is not my first time to go to see this web site, i am visiting

this site dailly and take good facts from here every day.

LikeLike