America used to be known as the land of free markets. That may have been the case in the past, but for many sectors, it no longer holds true. In The Great Reversal: How America Gave Up On Free Markets, Thomas Philippon makes the case that since 2000, Europe and America have switched places. America has abandoned many of the policies and practices that make markets freely competitive while Europe, through its efforts to create a single market, has implemented policies to reflect what American markets used to be.

Consistent with the views of Adam Smith, Philippon argues (below) that free markets feature competitive forces that inhibit the ability of businesses to obtain market power and thus economic rents. (See my previous post).

“I believe that markets are free when they are not subject to arbitrary political interference and when incumbents are not artificially protected from competitive new entrants. Keeping the markets free sometimes requires government interventions, but markets are certainly not free when governments expropriate private property, when incumbents are allowed to suppress competition, or when they successfully lobby to protect their rents.”

In The Great Reversal, Philippon makes three arguments:

- Competition has declined in many sectors in the U.S.

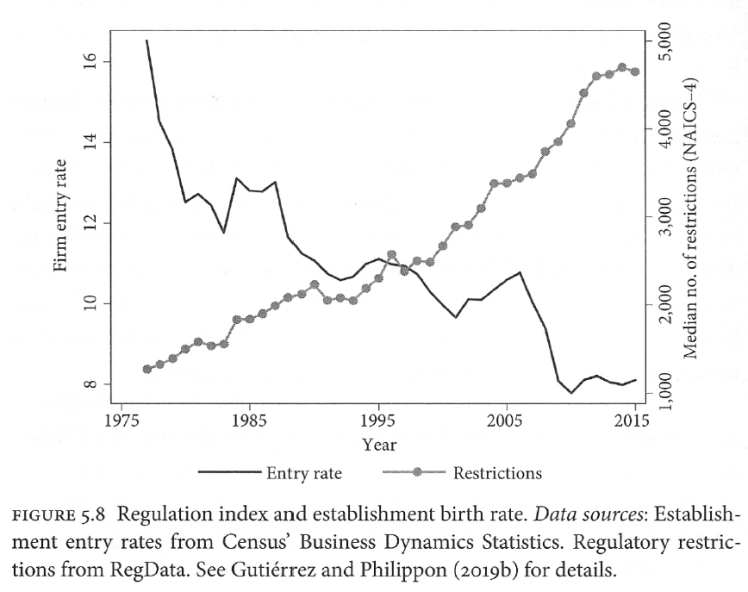

- Reduced competition can be largely explained by public policy choices influenced by business lobbying and campaign contributions. The result as shown below: increased entry restrictions on firms and, thus, reduced entry of new firms.

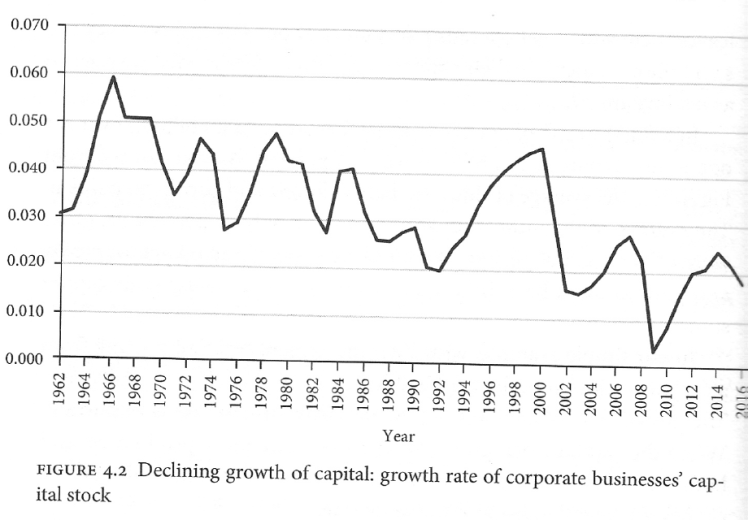

- As a result of reduced competition, the U.S. economy has experienced lower wages, less investment, lower productivity growth, and higher income inequality than it otherwise would have. For example, Figure 4.2 shows the decline in the growth of capital.

The book features four separate parts which Philippon draws upon in the concluding section to highlight three fundamental principles needed to construct and sustain truly free markets.

- “Free entry, always and everywhere” – Financial distress of particular companies should never be used as a basis to allow consolidation.

- “Governments Should Make Mistakes Too” – Regulators will make mistakes since they are human; however, regulation is necessary for the maintenance of free markets. The mistake regulators should not make is yielding to the rent-seeking interests of firms in those industries that they are charged to regulate.

- “Product Transparency, Privacy, and Data Ownership” – To sustain free markets, the U.S. needs to be part of an international consensus, at least among high income countries, that ensures priority for transparent prices and quality information, privacy for individuals, and data ownership by individuals. Consumers need to know what they are paying, why they are paying, and if they are not paying (such as on internet sites in general and social media websites in particular), which part of them is being sold.

The first part of the book makes the case for the rise of market power in the United States and its negative influence on prices, productivity, and income inequality. The two figures displayed above provide some of the evidence. In addition, in the below table, Philippon shows how wage rate differences among people with different educational backgrounds has widened in recent years. Note in particular the last row in the table which shows that the rise in the wage premium for those with graduate degrees has almost doubled since 1980 relative to those without a college degree.

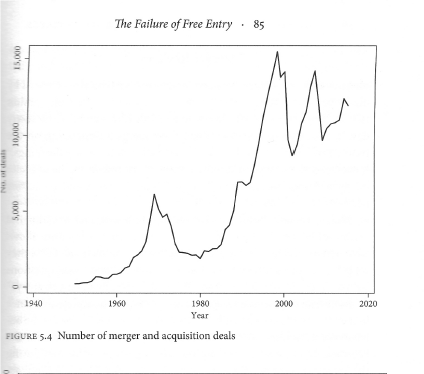

Consistent with the decline in the number of new entrants, the figure below shows that the number of merger and acquisition deals has burgeoned from the late 1990s onward. This is consistent with reduced anti-trust enforcement.

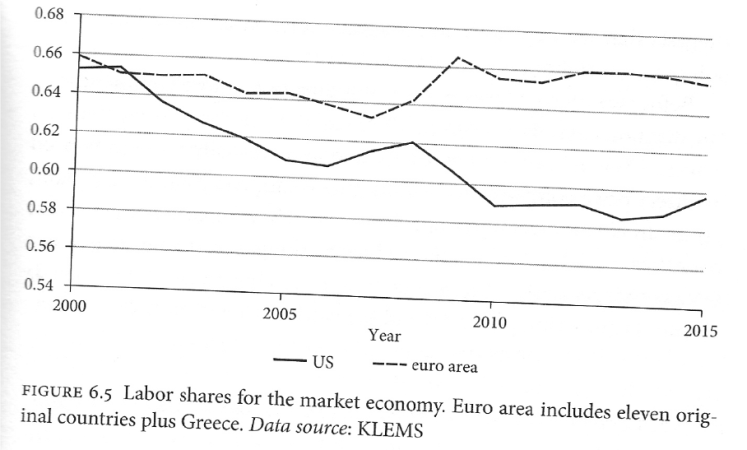

In the second part, Philippon draws on the character of European markets since 2000 to make the point that Europe has adopted free market principles and practices at the same time that the U.S. has abandoned them. Why did the U.S. abandon these practices in many markets and Europe adopt them? Philippon argues that large US firms have channeled their profits into building barriers to entry rather than to increasing the value of what they produce. In contrast, the creation of a single market in Europe has led to a consensus among European nations that no one country’s firms should dominate the single market; thus, barriers to entry of new firms, especially in the airline and telecommunications industries, have plummeted, and entry has surged with lower prices and better quality products and services as a result. Furthermore, labor’s share of national income in the US has fallen markedly, while in Europe, labor’s share has remained relatively stable.

In part three, Philippon demonstrates how large companies have devoted increasing amounts of funding both to lobbying and supporting candidates who assist them in building barriers to the entry of new competitors and to taxpayer support for many firms that would not be viable without it. Note how the number of politically active firms in the S & P 1500 has risen since the mid-1990s with almost half active politically.

In the final part, Philippon devotes attention to how specific industries have consolidated and the implications for consumer welfare. He highlights how entry barriers and technological improvements in the financial services sector have led to increased wages for highly skilled individuals but not lower costs for consumers. In the increasingly inefficient and inequitable health care sector, Philippon cites how low productivity improvement, hospital consolidation, and restrictive contracts put the US at the top of the cost table yet 28th (tied with the Czech Republic) in terms of access and quality. Philippon then turns his focus to recent “superstar” companies such as Google, Amazon, Facebook, Apple, and Microsoft. He notes that there have been significant benefits from the rise of these companies (good concentration) but that in the last decade they too have devoted an increased share of their earnings to lobbying Washington, which may already have generated anti-competitive results (bad concentration.)

Competition not only helps deliver quality goods and services at efficient prices to consumers; it also puts pressure on existing companies to continue to improve their products and deliver value to their customers. Without such pressure, as Philippon clearly shows, companies will not invest their gains to further improve their attractiveness to consumers. Instead they devote those resources to rent seeking for their executives and owners by lobbying politicians and regulatory agencies as well as contributing to the campaigns of those politicians who will help them protect their rents and viability. Such practices have led to both reduced growth in productivity and increased income equality. If these trends are to change, public policy makers in the U.S. will need to devote attention to the free market principles and practices that were commonplace for much of the second half of the 20th century.