Inflation, Government Spending and Modern Monetary Theory

On Tuesday, November 16th, I was a guest on Josh Dukelow’s Fresh Take program . We discussed a variety of topics related to inflation including governmental spending and modern monetary theory. Since I put together a set of notes for the program, I decided to take this opportunity to share my thoughts with those who follow this blog. The central question posed in the program, as in much discussion of national policy, can be stated as follows: Are current inflationary trends temporary (or transitory) or are they likely to be sustained for an extended period (of, say, at least one to two more years?) In my view, sustained inflation is the more likely prospect.

My Fresh Take interview was divided into three blocks (starting 55 minutes into the program linked above.) The first block sought to characterize inflation in general and ask whether the current information suggests an inflation problem.

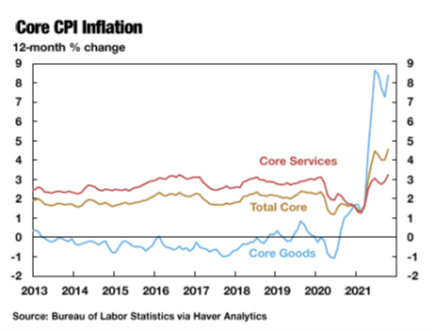

I characterize an inflation problem as one in which there exists a substantial, sustained increase in the average level of prices of goods and services; that is, one cannot assume price stability. Historically, substantial tends to mean 3% or greater; however, the Federal Reserve has set a target of 2% on average as consistent with stable prices. Sustained refers to the above growth rates for at least one year. A focus on the average level of prices means that one must look beyond rises in prices for various forms of energy, used cars, housing, or particular foods to aggregate measures of price. Current evidence from a variety of indicators suggests a 3.5% to 8.5% rise in prices over the past year, which certainly suggests an inflation problem. For example, see the Personal Consumption Expenditures Deflator and Consumer Price Index graphs below.

The second block of the program was devoted to discussion of the nature of governmental expenditures and their effects on inflation.

In response I categorized governmental expenditures into four different types.

- that designed to bring GDP back to its long term potential level – The Cares Act (2020) and the American Rescue Plan Act (2021) match this characteristic. Such policies reflect a Keynesian public increase in demand in response to a significant decline in private sector demand for goods and services. Given the assumed excess capacity in the economy, these policies should have a negligible effect on inflation.

- that designed to increase long term GDP – The recently passed $1.2 trillion Infrastructure Investment and Jobs Act (November 2021) provides a good example. The law highlights provisions to update U.S. roads, bridges, water systems, ports, and internet components. Many of these improvements could lead to significant increases in productivity, thus, long term growth in GDP. If increased productivity results, then some prices could fall and inflation rates would decline.

- that designed to transfer income from one group to another –The Build Back Better Program presently under discussion in Congress has many components that reflect taxing well-off individuals and companies and providing funding for low and middle income families. Some provisions, such as support for the purchase of day care services, might enable U.S. residents to become more productive, but, given the information available, most of the bill aims to transfer income from well-off to less well-off people. As one of the purposes is to put funds in the hands of those likely to spend it, significant potential for inflation exists.

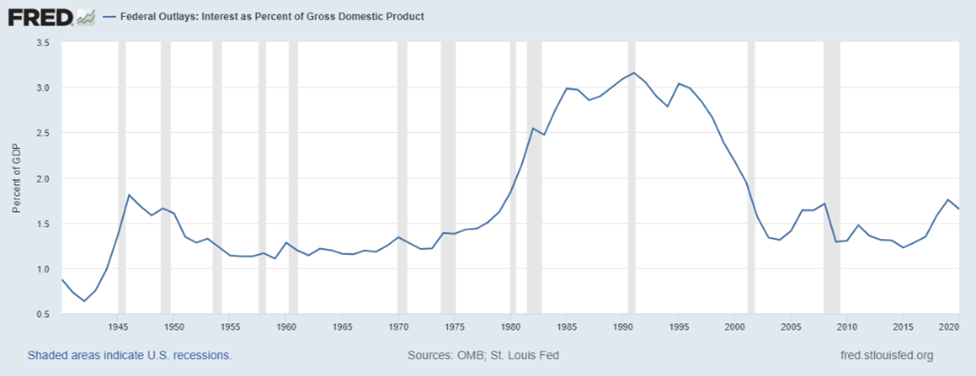

- finally, that required to pay the debt service – interest plus matured debt. Since matured Treasury securities tend to be rolled over into new debt, only interest payments find their way into budget documents. Given the low interest rates on Treasuries, such payments have not (yet) put a heavy burden on the economy – roughly 1.5% of GDP. It’s near its high point of the past 20 years but well below what it was in the 80s and 90s.

Related to the above spending, the ratio of existent federal debt ($28.5 trillion) to GDP has now reached more than 125% with debt held by the public ($22.4 trillion) almost equal to GDP (98%.) Debt held by foreign entities has reached $7 trillion with Japan and China each holding more than $1 trillion of US Treasuries. China’s holdings have dropped from $1.8 trillion in 2015 to just over $1 trillion today. Of course, if the Chinese government chose to sell a large portion of its holdings onto the market at one time, two things would result: the value of Chinese holdings would fall markedly and interest rates in the U.S. would rise.

To the degree that increased spending, funded by public debt, expands demand faster than it expands supply, one could express inflationary pressure.

The third segment of the program focused on Modern Monetary Theory (MMT) as well as the consequences of sustained inflation above 3%. First, I summarized MMT which I discussed on Fresh Take a couple of years ago and addressed in a blog posting in 2019. Here’s a brief version of that posting.

- Countries that print their own currencies need not default on their debt.

- Inflation can be controlled by raising taxes or cutting spending sufficiently to soak up excess money, which won’t be necessary until the economy reaches its capacity.

- MMT advocates typically cite some measure of the full employment rate of unemployment as their measure of full capacity: typically, an unemployment rate around 4% in the U.S.

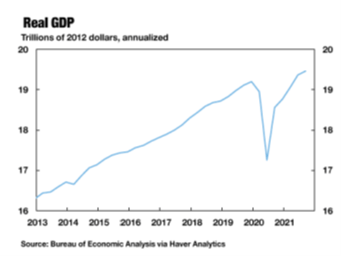

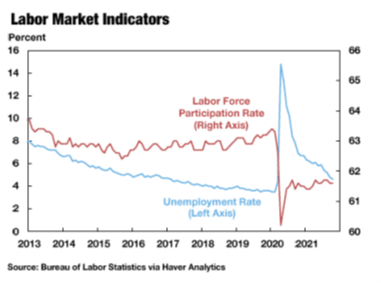

I have argued that this theory is neither modern, nor particularly monetary, and that it does not represent a coherent theory of the macro economy. In short, MMT can’t cancel the notion that if the growth in demand (from whatever source) exceeds the growth in supply, inflation will result. Furthermore, as exists currently and in contrast with MMT and traditional Keynesianism, inflation may be generated prior to an economy reaching what might commonly be viewed as full employment or potential GDP. As of the end of the third quarter of 2021, GDP remains roughly 2% below its long term trend and, the unemployment rate is still above what many view as full employment. Of course, the labor force participation rate has not returned to its pre-covid level as shown in the graph below. Nevertheless, inflation has exceeded stable rates for the better part of a year.

There is substantial disagreement regarding what has driven inflation up to its current rate. Cecchetti and Schoenholtz summarize the multiple factors that have played a role in addition to monetary expansion including:

- Expansion of governmental spending (as noted above)

- Shifts in the composition of demand from services to goods

- Firms’ spending to replace inventory and ensure they have sufficient goods if future supply bottlenecks result

- Reductions in labor force participation

- Pandemic-induced increases in the cost of labor, especially for in-person services

- Bottlenecks in supplies

- The reallocation of capital and resources to accommodate shifts to remote work

The first three have led to increased demand, while the rest have reduced supply or increased its cost. Some of these factors are likely to persist for some time; thus, inflation above 3% is likely to persist.

So how does a higher inflation rate matter? When inflation rises above a low and stable rate (such as the Fed’s 2% rate target), it affects decision-making. In particular, expected inflation will also rise and be reflected in various domestic markets through changes in interest rates, wage rates, and various other contracts. A recent New York Fed survey of consumer expectations indicated that the 1 year median expected inflation rate had risen to 5.7% and the three year median expectation was 4.2% per year. In inflation-adjusted terms, Treasury securities and certificates of deposit, for example, would yield negative purchasing power since the interest earned would be less than the expected rise in prices of goods and services. As a result, many households and firms would divest their holdings and either buy other assets (such as bitcoin) or bring forward purchases that they believe will become more costly in the future.

Furthermore, if foreign entities view US Treasuries as either insufficiently secure or offering a lower inflation-adjusted (real) return than other similar assets, they would sell them, and real interest rates would rise.

Result: Given that inflation has risen above its low and stable rate for the past decade (that is 2% or lower), it now matters and will be taken into account in many financially related decisions. Even the Federal Reserve Board (FED), which has been biased towards employment related measures over the past decade, won’t stand still. For example, FED Vice Chair Richard Clarida recently argued:

But let me be clear on two points. First, realized PCE [Personal Consumption Expenditures] inflation so far this year represents, to me, much more than a ‘moderate’ overshoot of our 2% longer-run inflation objective, and I would not consider a repeat performance next year a policy success. Second, as always, there are risks to any outlook, and I and 12 of my colleagues believe that the risks to the outlook for inflation are to the upside.

Furthermore, any constructive move to decarbonize the US or the world economy will be disruptive to goods and labor markets; thus, supply growth will have to slow, at least in transition. In response, some income transfers will be made, especially to help some low and middle income families who, at least initially, will be worse off. These supply constraints matched with demand support will yield an inevitable result: inflation significantly above the 2% viewed as consistent with price stability.

Finally, inflation tends to redistribute income and purchasing power from lower and middle income residents to higher income residents since the latter group has more means and information to protect themselves against such reductions in the purchasing power of their income.

One thought on “Inflation: Temporary or Sustained ?”