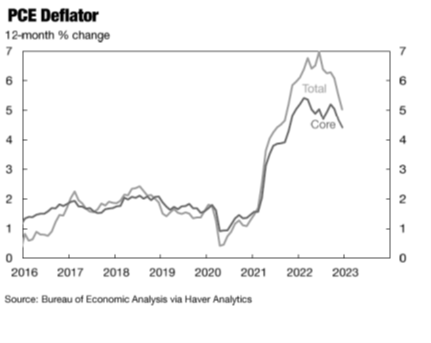

In November 2021, after being a guest on Josh Dukelow’s Fresh Take program, I posted two related pieces: one on whether inflation was temporary or not and a second on the role of monetary policy. It’s time for an update, especially since the inflation rate has risen significantly since November 2021 (see the below chart) and because the Federal Reserve has increased its target interest rate from a range of 0% to 0.25% to a range of 4.50% to 4.75% with further increases on the horizon.

Some analysts have argued that further monetary tightening is either unnecessary or counter-productive. For example, Jeffrey Sommers argued that prices for items such as fuel, food, and computer chips have come down to acceptable levels; so why continue to “fight” an unnecessary battle, given the potential negative consequences for economic growth and employment. In a related view, Joseph Stiglitz has argued that inflation in the past two years has been the result of supply constraints and supply chain disruption and that both have now eased.

In my view, both of these views say little about what inflation will be in the next couple of years. Since monetary policy works with a substantial lag in terms of its impact on spending (6 to 18 months), analysts need to look forward rather than in the “rear view mirror.” There are a host of factors that suggest the upward pressure on prices will continue. My intent in this posting is to indicate such factors, with one or two relevant references, rather than to spell out a detailed argument that would be much too long for this posting.

So, here’s the list:

- The U.S. has been engaging in deglobalization efforts to reduce the potential dependence on unreliable sources (including but not limited to China.) As a result, the U.S. will depend much more on domestic production than on imports. In terms of intermediate goods, this will lead to upward pressure on costs and, thus, on domestic prices. For discussion of globalization trends, check out the recent Peterson Institute event on globalization. In a related Deutsche Bank piece, Rebecca Harding has summarized how reduced trade and inflation are connected. “As I have observed before, trade, in that it has been used strategically in foreign policy, has been weaponised. Inflation is the result and this affects everyone. There are levers that can be pulled through trade to make it a force for de-escalating these pressures and if we don’t use them, the situation could worsen still. Is that really a price worth paying?”

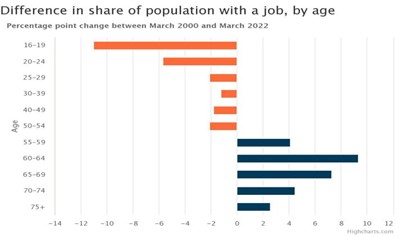

- Demographics in the U.S. suggest an aging population with the working population shrinking relative to the dependent population. With relatively fewer workers providing goods and services to a growing population, labor markets will become tighter. Unless productivity increases at the same rate as employment falls, costs must rise; for a given level of demand, prices will rise to compensate. The fall in the labor force participation rate, especially among those under 55, reinforces the demographic implications just noted. See below chart and the related article in the Conversable Economist. Furthermore, unit labor costs – the ratio of labor cost per hour to output per labor hour – have risen and are likely to continue to rise with subsequent rises in prices. For 2021 and 2022, the Bureau of Labor Statistics reported that unit labor costs in the business sector rose by 8.3% and 8.4%, respectively.

- The pandemic has changed a variety of factors including the work-leisure mix and consumption patterns. Furthermore, supply chains are not likely to return to what they were prior to March 2020. A combination of the deglobalization/protectionism trends along with trade realignments as a result of the war in Ukraine suggests the US economy will not return to its pre-pandemic character. To the degree that the cost of such adjustments doesn’t reflect productivity improvements, prices must inevitably rise.

- Household spending and related credit expansion suggests demand will continue to increase. For example, the Federal Reserve reports that consumer credit outstanding has risen from $4.2 trillion in 2019 to $4.8 trillion in December of 2022.

Yes, the Federal Reserve needs to be concerned about a potential recession and its implications for employment. The January employment report of a net increase of 517 thousand jobs, well above the roughly 100 to 150 thousand needed to sustain employment consistent with labor force growth, suggests that a recession is not on the horizon. Furthermore, vacancies continue to significantly outpace the number of unemployed workers. The Bureau of Labor Statistics recently reported the following:

“At the national level, the unemployed people per job openings ratio was 0.6 in December 2021, compared with 1.6 a year earlier. A ratio of 1.0 means there is a job available for every unemployed person. Ratios less than 1.0 signal tighter labor markets in which firms have more job openings than there are people looking for work.”

Even though the yield curve on U.S Treasuries (10 year interest rate minus the 3 month interest rate) has been negative for the past 8 months, a strong indicator of recessionary forces, employment trends remain inconsistent with this signal.

Stiglitz and others point out the cost of continued monetary tightening could be recession, a serious concern. The advocates of monetary easing, however, don’t address the cost of not bringing down inflation. We know that the well-off can protect themselves against inflation much easier than can the less well-off. Prior to mid-term elections in 2022 inflation was Americans’ top public policy concern. Furthermore, the New York Federal Reserve Bank’s February 13, 2023 Survey of Consumer Expectations observed that households expect an inflation rate of 5% for the coming year.

Stiglitz correctly argues that monetary policy won’t address the inflation generated by negative supply shocks; in fact, a tightening of monetary policy (as reflected by a rise in the FED’s interest rate target) would yield both higher prices and lower output and employment. Factors 1 (deglobalization) and 2 (demographics) above are supply-side factors; however, a tighter labor market, in light of increased inflation and expected inflation, would lead to a further boost in wages and then to prices that could sustain or even increase the inflation rate. Factor 3 (pandemic effects) suggests influence on both the supply side (a change in household decisions about market work versus non-market labor) and demand side (household consumption patterns.) Factor 4 (increased borrowing) clearly represents a demand-side push.

Bottom line: both supply and demand side factors are at work to push price trends higher, which will make it difficult to bring inflation down to an acceptable rate. Higher interest rates will help limit the “knock-on” effects on inflation of the four factors cited above. Of course, monetary policy is not the only instrument to address inflation; fiscal policy and productivity-related policies also deserve attention.

I’ll conclude this piece with a repeat (from a previous blog posting) of the wise words of my former mentor Edward Foster at the University of Minnesota from his 1980 “Who Loses From Inflation?” article.

The most serious costs of persistent inflation may be that it destroys our confidence that society can solve its problems and creates fear that our social contract is falling apart. Coupled with the fear is resentment, based on suspicion by many that inflation treats them unfairly. Those who lose are all of us who share those fears and frustrations.