Currency exchanges rates between any two countries are determined by a variety of factors including their balance of trade and payments, capital flows (both restricted and unrestricted), and monetary policies. In a recent posting on Conversable Economics, Timothy Taylor argued that “all exchange rates are bad” (meaning that they generate some negative consequences.) Although this posting does not take issue with Taylor’s arguments (and will pose them shortly), I conclude that there is no one optimal set of exchange rates, since for any given set, there will be winners and losers, and trade-offs among policy objectives must be made. In short, there is no unique way to determine which exchange rate between countries is “just right.”

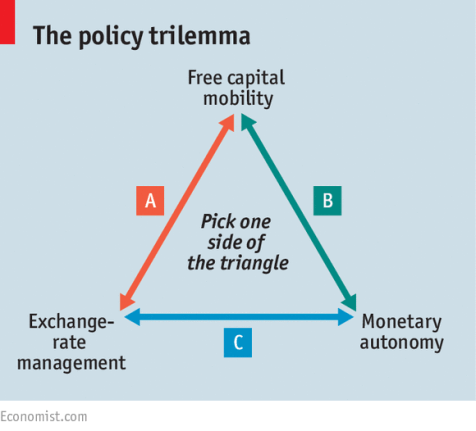

Exchange rate policy and monetary policy are intrinsically linked. Countries face what has been called the “Impossible Trinity” or “Trilemma”; they can only choose two of the following: independent monetary policy (setting short term domestic interest rates), fixed exchange rates, and open capital markets. Thus, a country’s desire to float, fix, manage, or abandon how the price of its currency relates to others depends critically on its views toward monetary policy and the flow of capital into and out of the country. Stated differently, to some extent, all countries manipulate their exchange rates by the judgments they make about the tradeoffs amongst the three choices.

There have been a variety of attempts to determine appropriate sets of exchange rates. The Economist posts its Big Mac Index each year, which determines how much existent exchange rates differ from the rate needed to have Big Macs cost the same everywhere. Such a set of rates satisfies those required for purchasing power parity (PPP); that is, currency exchange rates in which goods would trade for the same price, after currency conversion, everywhere. Purchasing power parity requires that currencies float until such price equilibria are achieved. The Organization for Economic Cooperation and Development (OECD) also produces a set of purchasing power parity rates; it’s most recent set was published in 2016. In contrast with the Big Mac index, OECD calculations reflect a basket of goods purchased by households, businesses, and governments. Since many goods and services are not traded between countries, purchasing power parity calculations are based on some specific assumptions about the weights of various traded goods. These weights, based on actual trades of goods and services, change over time as relative prices change. The same can be said about exchange rates; they are a relative price which changes as the demand for and supply of various currencies change.

In contrast with PPP approaches, William Cline at the Peterson Institute twice each year estimates a set of Fundamental Equilibrium Exchange Rates (https://piie.com/publications/policy-briefs/estimates-fundamental-equilibrium-exchange-rates-november-2016) based on a model that determines what the exchange rate would need to be to bring the non-oil trade balance (NOTB) for a country to a particular rate. Cline uses a ratio of the NOTB to GDP ratio of -3% as his target for the U.S.

In the table below, PPP based calculations show that the dollar is overvalued relative to the euro, yen, pound, and renminbi. Cline’s calculations show that exchange rates are approximately “just right.”

| Exchange Rate Equilibrium | Big Mac Index – 1/12/2017 adjusted for GDP/capita | Purchasing Power Parity – OECD – 2016 | FEER – W. Cline October 2016 |

| US $ vs. German € | € undervalued by 1.1% | € undervalued by 14.4% | € overvalued by 0.8% |

| US $ vs. Japanese ¥ | ¥ undervalued by 19.9% | ¥ undervalued by 6.6% | ¥ undervalued by 3.3% |

| US $ vs. British £ | £ undervalued by 18% | £ undervalued by 6.9% | £ overvalued by 0.5% |

| US $ vs. Chinese RMB | RMB undervalued by 6.5% | RMB undervalued by 47.0% | RMB overvalued by 0.7% |

Tim Taylor argues that all exchange rates have some negative consequences:

- If they are too low, they hurt net importers.

- If they are too high, they discourage foreign direct investment and net exporters.

- If the rates are too volatile, then the increased uncertainty will reduce economic activity.

- If they are too stable, they can easily deviate sharply from what is needed to balance supply and demand for currencies.

As Taylor puts it, “the bottom line is clear as mud. Exchange rates are bad if they move higher or lower, or moving, or stable.”

Furthermore, in the short run, balance of trade differences have very little influence on exchange rates. The $21-24 trillion of annual world trade in goods and services is swamped by the $5.1 trillion per day trades in foreign exchange markets with roughly 7 out of 8 exchanges involving the dollar on one side. The value of the dollar as the world’s primary reserve currency matters more than other currencies; furthermore, commodities such as oil are traded in dollars, not in other currencies. This presents US policy makers with a dilemma (sometimes called the Triffin Dilemma.) They could focus on supplying sufficient dollars to facilitate world trade or on how the supply of dollars in circulation affects domestic interest rates and markets. Even the U.S. can’t escape the Trilemma.

Based on recent IMF reports, Taylor points out that countries choose a variety of different strategies regarding which type of exchange rate regime to adopt. Roughly one-third of the countries (including the U.S.) in the world allow their exchange rates to float, and, thus be largely driven by daily currency trading. Another one-eighth of the countries peg their exchange rates to that of another country or adopt the currency of that country (e.g., Ecuador uses the U.S. dollar as its currency.) The remaining countries, which constitute more than half the countries in the world, manage how much their currencies float against the currencies of their main trading partners. Attempts to place all countries on one set of exchange rates based on the 1944 Bretton Woods agreement existed until international payment imbalances caused the U.S. to end its foundational role in 1971. For history buffs, the end came in 1971 when Treasury Secretary John Connally informed his European counterparts at the G-10 conference in Rome that “the dollar is our currency, but it’s your problem.” For any fixed set of exchange rates to be just right – whether tied to gold, the dollar, the euro, or the RMB – relative prices and preferences for both goods and services and currencies would need to be stable over an extensive time period. This would indeed be a very heroic assumption, and, thus, a poor guide to setting policy.

Great readd

LikeLike